The 125000:1 Problem in Indian Investing

Is it the end for RIAs in India's equity markets?

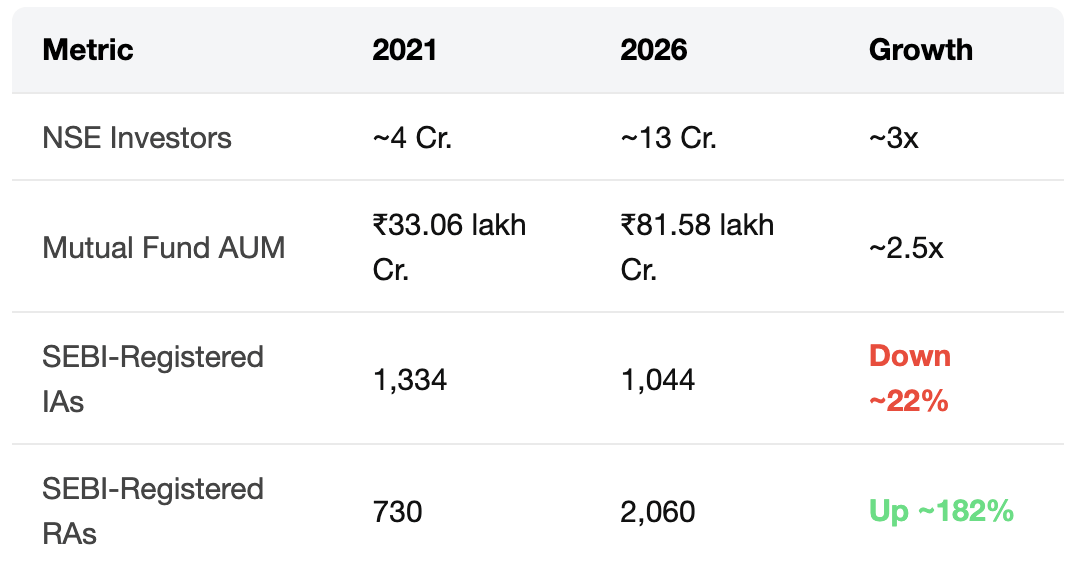

Between 2021 and 2026, the number of NSE investors jumped from ~4 crore to ~13 crore, while mutual fund assets surged from ₹33 lakh crore to ₹81.6 lakh crore.

Yet one part of the ecosystem barely grew: Investment Advisors.

Research can be distributed to thousands of subscribers at once, but advice requires understanding a client’s goals, risk profile and existing portfolio before making recommendations.

Naturally, scaling personalised advice remains a challenge in India.

The Advice Gap

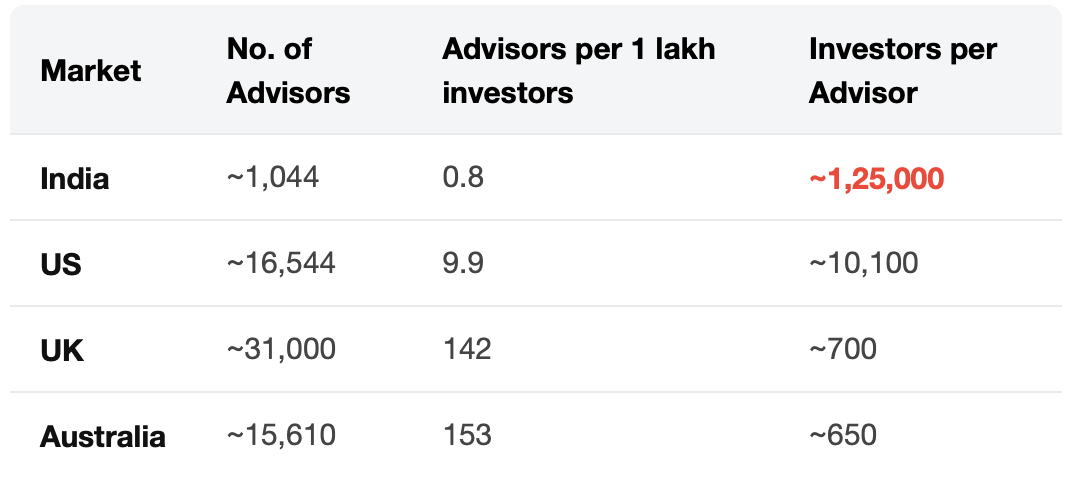

India has 125x lower advisor density than global benchmarks.

Just 1 advisor for every 1.25 lakh investors! As more Indians enter the markets, access to personalised advice is not expanding at the same pace.

So, why has the advisory model struggled to attract and retain advisors despite rapid growth in investors, assets and market participation?

The Economics Mismatch

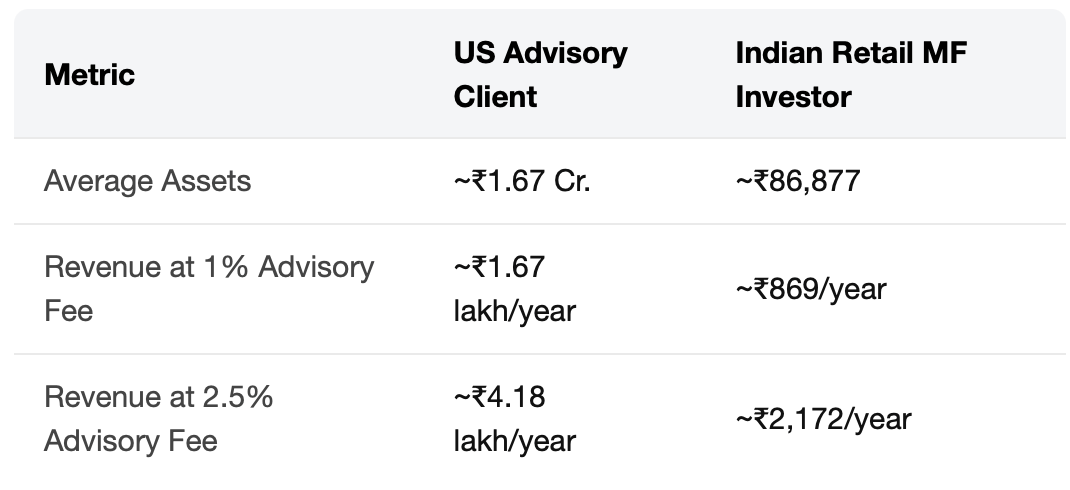

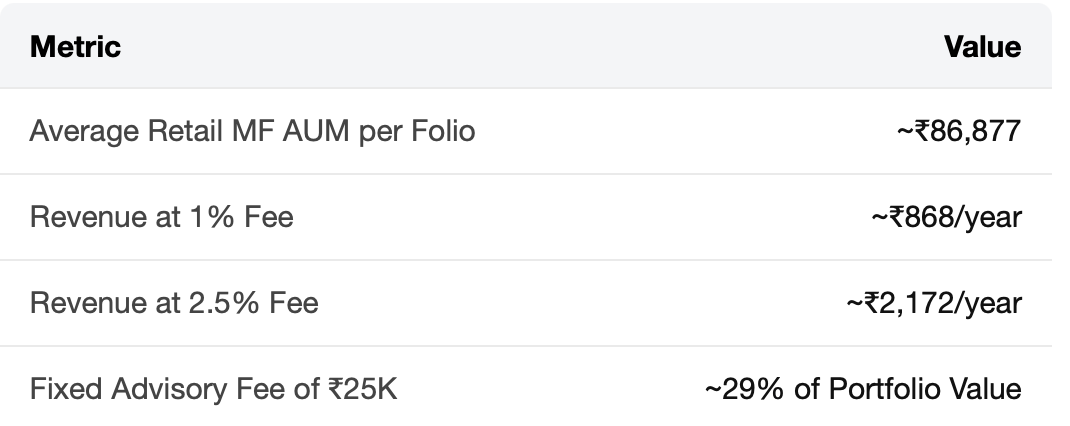

The biggest reason Indian RIAs do not scale is the mismatch between service cost and client portfolio.

Personalised advice needs time, documentation, risk profiling, portfolio reviews, suitability checks and regular follow-ups. But the average Indian retail portfolio is too small to pay for this service meaningfully.

The US shows how advisory can scale when portfolio sizes, fee collection and execution support the model.

Advice is often linked to larger household wealth pools and retirement assets.

AUM-based fees are widely accepted, and fees can be deducted from client’s account.

Custodians handle asset custody, reporting and fee collection.

Many advisors can manage portfolios under agreed mandates, including rebalancing and implementation.

Plus, most RIAs are not giant institutions in the US.

92.8% had 100 or fewer employees.

Individual-focused firms averaged just 8 employees.

Yet they managed roughly ₹4,000 crore in assets on average.

Larger portfolios, accepted AUM fees, and stronger execution support allow even small advisory firms to operate at a meaningful scale.

India’s IA model is narrower. RIAs primarily provide advice, while portfolio management and execution typically require a PMS or similar licence.

Retail-focused advisory businesses in India face a much tighter economic equation.

Thus Arises the Affordability Paradox

For advisors, qualification requirements, suitability assessments, audits, record-keeping and disclosure obligations create fixed operating costs regardless of whether an advisor serves 50 clients or 5,000.

For investors, paying separately for advice can feel expensive relative to portfolio size.

The result:

Higher Compliance Requirements ➡️ Higher Fixed Costs ➡️ Higher Fees Needed ➡️ Retail Investors Resist Paying ➡️ RIA Growth Stalls

This naturally pushes many advisory businesses towards affluent investors, larger portfolios or technology-led models.

RIAs: Sandwiched Between Two Larger Ecosystems

At the retail end, mutual fund distributors dominate onboarding and SIP distribution. Investors can begin investing without having to write a separate cheque for advice, since the cost is embedded in the product structure.

The scale achieved by the distribution ecosystem is substantial.

The MFD industry is also concentrated, yet it has produced far more scalable businesses than the RIA model.

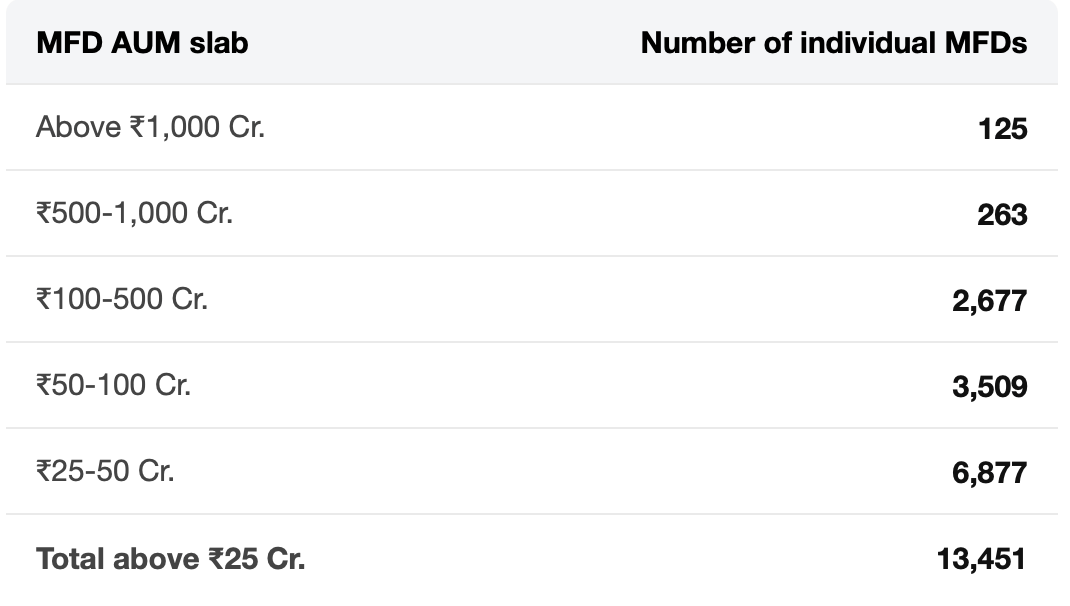

Out of roughly ~1.8 lakh individual MFDs, only about 13,451 manage more than ₹25 crore of assets, meaning just 7.5% operate at a meaningful scale.

Even within this concentrated group, more than 3,000 individual MFDs manage over ₹50 crore, while the entire SEBI-registered IA base stands at just 1,044.

At the other end of the market, affluent investors often seek portfolio management, execution, reporting, lending solutions, estate planning and access to specialised products.

This leaves RIAs serving a narrower segment between the two.

Mass Retail (~1.8 lakh MFDs) ← RIAs → HNIs (PMS & Wealth Platforms)

The Scaling Problem

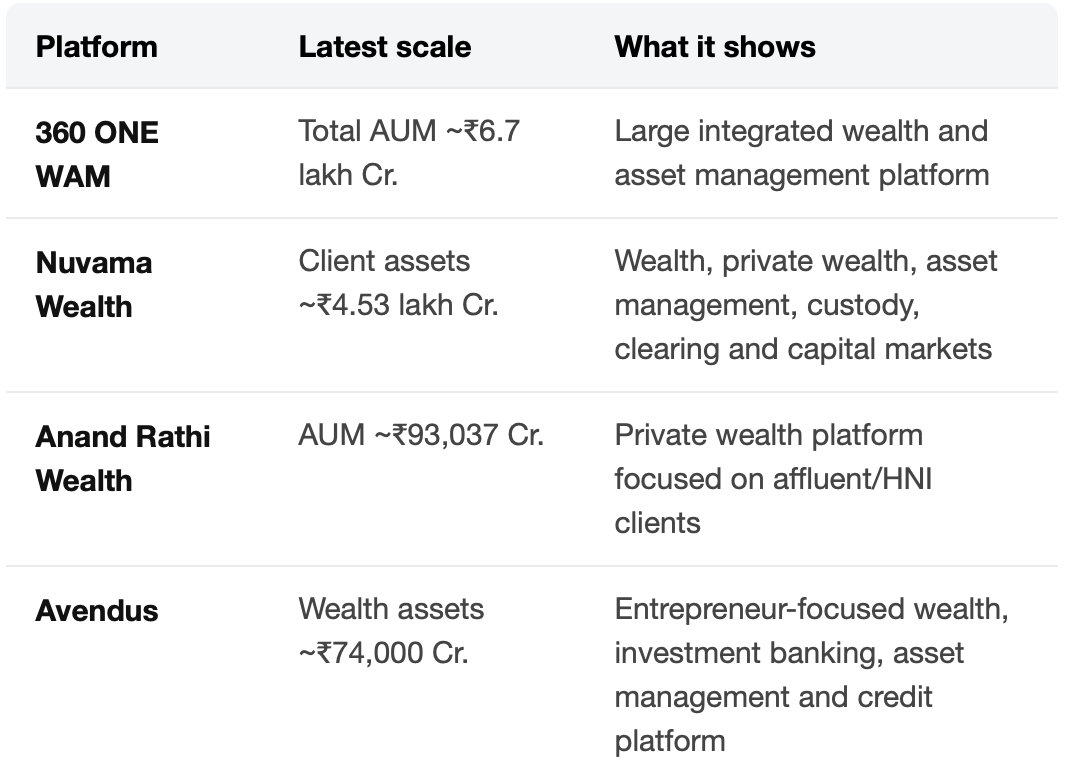

Another clue lies in where the scale exists. India’s largest advice-linked businesses are not scaled-up boutique RIAs, but rather integrated wealth platforms.

These firms function like integrated wealth platforms.

A wealthy client may need portfolio advice today, lending solutions tomorrow, PMS or AIF access later, and estate planning over time. Large platforms can serve multiple needs under a single relationship.

This creates three advantages.

Cross-selling: Offering multiple services creates multiple revenue streams from the same client.

Operating leverage: Research, compliance, technology, etc., are largely fixed costs. A platform managing lakhs of crores of client assets can spread these costs across a much larger base, while a boutique RIA faces similar compliance intensity with far fewer clients.

Talent leverage: Clients often follow trusted RMs. Larger platforms can attract and support RM teams through stronger brands, research and product capabilities, while boutique RIAs are usually more dependent on the founder’s personal brand.

As a result, scale naturally gravitates toward larger wealth platforms.

Why Boutique RIAs Struggle

Time-intensive advice: Understanding goals, risk profile, existing investments, tax position and investor behaviour requires significant effort, while smaller portfolios often generate limited revenue.

Compliance burden: Risk profiling, suitability checks, disclosures and audit trails must all be maintained, often by the same small team handling advisory and client servicing.

Founder dependency: Clients usually trust the founder’s judgement, creating a natural ceiling unless advice can be standardised and delivered consistently across a larger team.

What Can Help

Focus on segments where advice has greater value, such as affluent families, NRIs, retirees, business owners and investors with complex portfolios.

Introduce minimum fees, minimum portfolio sizes or tiered service models to protect service quality.

Use shared technology and compliance tools to reduce operational overhead.

Build processes and training systems that allow advice to scale beyond the founder.

So, Are RIAs Unimportant?

No. They serve a role that distribution-led and product-led models cannot fully replace.

Investors with complex portfolios, retirement needs, asset allocation decisions or behavioural challenges often benefit from personalised advice tailored to their situation.

RIAs are fiduciaries by law. Their advice is not tied to commissions or product sales, and they are expected to act in the client’s best interest. In many ways, they provide a perspective that starts with the investor’s situation rather than the product being offered.

India has largely solved access to investing. The next challenge is improving the quality of decision-making.

Finology’s Exclusive Updates

Article Update: Lessons from Rajesh Exports

Beyond the headlines, the Rajesh Exports case offers valuable lessons in financial statement analysis and corporate governance.

Our latest article explains the allegations step by step and explores what investors should pay attention to when evaluating companies.

Game Time!

The Cost of “Free” Advice

Many investors don’t pay directly for advice. Instead, distributors earn commissions from the products they recommend.

That’s all for today!

Hope this edition felt useful and worth your time.

If it did, drop a like and comment how. Also, if you’d like us to cover more (or less) of such content, do tell. We love to get better for our people.