DeepScan #2: ICICI AMC

What happens when leadership comes from balancing growth and stability?

Hello,

This is the second edition of our series.

DeepScans are an extension of the research process we follow at Finology 30. While not every company we analyse becomes an investment candidate, every DeepScan is an opportunity to understand how a business works.

In the previous one, we covered the asset management industry, the sector’s long-term opportunity, and a business analysis of HDFC AMC. I suggest you read that piece first to understand the industry dynamics better and be better equipped to consume this one.

This week, we are looking at ICICI Prudential Asset Management Company Ltd., India’s second largest AMC and HDFC AMC’s closest listed competitor.

At first glance, both businesses may look similar. Both are large AMCs, both have strong parentage, and both benefit from India’s rising mutual fund participation.

But once we go deeper, you’ll see how each is different in its own way. So let’s begin!

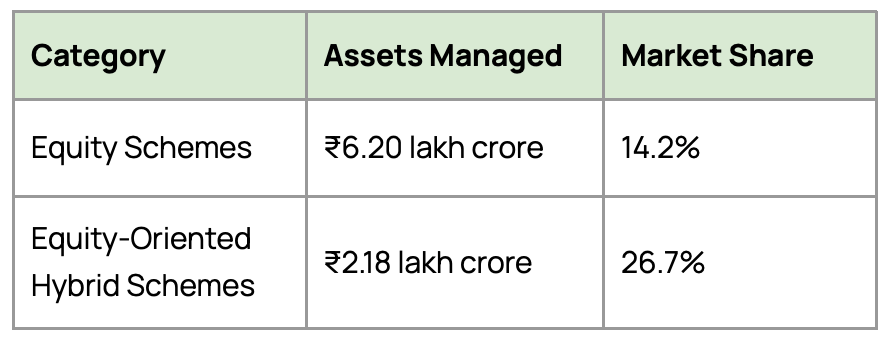

As of March 2026, the company managed ₹11.05 lakh crore of mutual fund QAAUM, giving it a 13.5% market share. QAAUM means quarterly average assets under management. Instead of looking at AUM on just one day, it shows the average assets managed during the quarter.

It smooths out sudden market moves at the end of a quarter and gives a cleaner view of the assets managed during the period. Since an AMC’s revenue depends on the average size and mix of assets it manages, QAAUM is a better measure of its core earning base than closing AUM.

More importantly, it had the highest market share in active mutual fund assets at 13.7%.

Its strength is even clearer in the higher-value categories.

ICICI Prudential AMC also had around ₹73,000 crore of alternates QAAUM, including PMS, AIF and Advisory.

This makes ICICI Prudential AMC a broader asset management platform, with leadership in mutual funds and expanding alternates business.

Now, when analysing bank-promoted AMCs, the first question an investor must ask is:

Is the business growing because its parent bank is aggressively pushing the product, or because the market actually wants it?

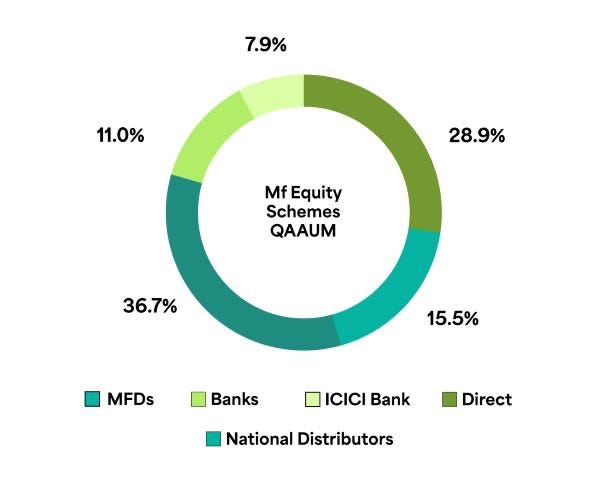

As of March 2026, ICICI Bank contributed only 7.9% of the company’s equity mutual fund AUM. Even after adding another 11.0% from other banking partners, the total bank channel contribution remains 18.9% of equity AUM.

The real engine is outside the banking channel. Take a look at this chart:

This means more than 80% of the equity book is coming from non-parent-led channels.

In comparison, HDFC AMC is less dependent on banks. In its equity-oriented AUM, HDFC Bank contributed 6.5%, while the total bank channel stood at 11.9%.

Banks can bring scale, but their sales depend on internal priorities, such as deposits, insurance or loans. MFDs and national distributors are not limited to selling one AMC’s products. They compare multiple AMCs and usually recommend funds based on performance, brand, product fit and client need.

So, if an AMC gets strong flows from these channels, it shows that investors and distributors are choosing the product on merit.

Technology is adding further operating leverage to this network. ~95.7% of total mutual fund purchase transactions were executed digitally. This allows the company to scale transactions and onboard customers without a similar increase in branch or employee costs.

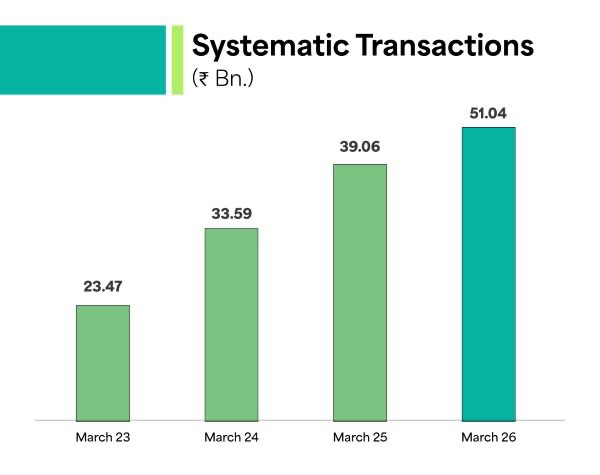

This distribution engine is also visible in recurring flows. Monthly systematic transactions, including SIPs and STPs, reached ₹5,104 crore in March 2026, up from ₹2,347 crore in March 2023, CAGR of 30%. This is broadly in line with the industry’s SIP growth of around 31% during the same period.

So, ICICI’s systematic flow engine is strong, but unlike HDFC AMC, it is not clearly outperforming the industry.

After building a strong retail mutual fund franchise, ICICI Prudential AMC is expanding into the HNI and institutional segment through its alternates business, which includes PMS, AIFs and offshore advisory.

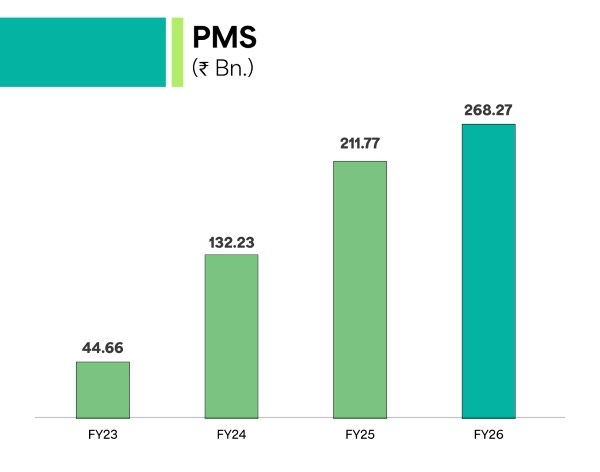

The PMS business is the traditional anchor of ICICI Prudential AMC’s Alternates platform. It mainly manages customised listed equity portfolios for affluent investors seeking more personalised strategies than those offered by regular mutual funds.

This segment has scaled sharply, with PMS QAAUM rising from ₹4,466 crore in March 2023 to ₹26,827 crore in March 2026, implying a strong 81.8% CAGR over three years.

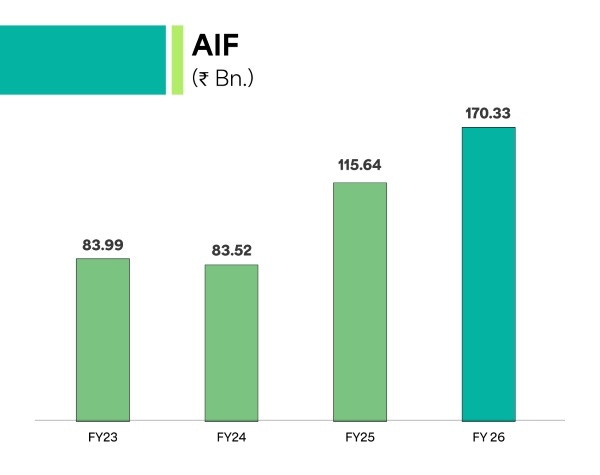

AIF is another important growth driver for the company. It allows the company to pool money from sophisticated investors and invest in areas such as private credit, real estate yield funds and early-stage private equity.

This segment has also scaled well, with AIF AUM rising from ₹8,399 crore in March 2023 to ₹17,033 crore in March 2026, implying a 26.6% CAGR over three years.

It has further strengthened its Alternates platform by acquiring investment management rights for certain AIFs from ICICI Venture, effective April 2026. This adds around ₹4,628 crore of fee-paying committed capital and brings capabilities in private equity, early-stage venture capital and affordable housing funds under the AMC’s direct control.

Under the offshore advisory business, the company provides investment advisory and management support to international investors, sovereign funds and global funds looking to invest in Indian markets, earning fee income.

It manages around ₹29,134 crore, earning a 0.33% yield. Together, PMS, AIFs and offshore advisory take ICICI Prudential AMC’s total Alternates QAAUM to around ₹72,995 crore, ~6% of its total managed assets

While HDFC remains strong in traditional mutual funds, ICICI AMC has built a much stronger position in the higher-yielding alternates space.

But the downside is that this revenue is less predictable than mutual fund revenue. Mutual fund fees largely come as a fixed charge on a large and diversified AUM base, supported by SIPs. PMS/AIF income is more exposed to market performance, HNI sentiment, performance fees, fund launches and exits. ICICI itself says PMS/AIF fees may vary significantly from period to period, depending on performance versus benchmarks or required returns, which is exactly the risk investors should watch.

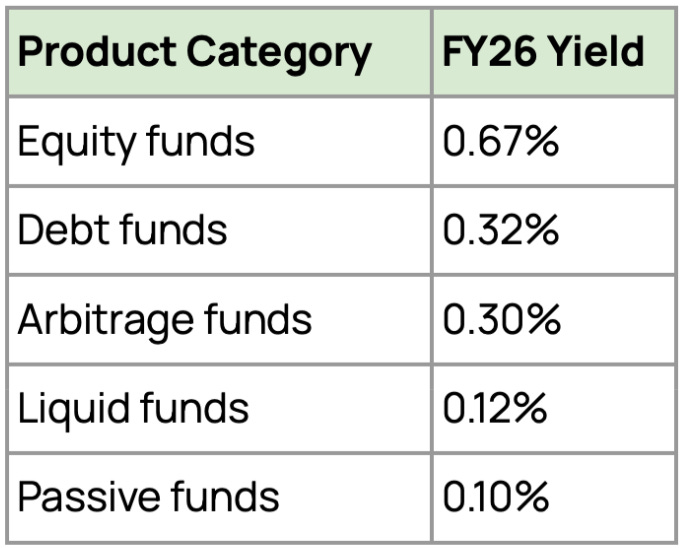

Mutual funds remain the core profit engine. They contribute ~91% of core operating net revenue, while alternates contribute ~7% and advisory services ~2%.

In mutual funds, equity, hybrid and other active products usually carry better economics than liquid or passive funds because they involve active management, product differentiation, distributor support and higher investor handholding.

For the AMC, Hybrid funds create stickier AUM because investors are less likely to panic and redeem during corrections.

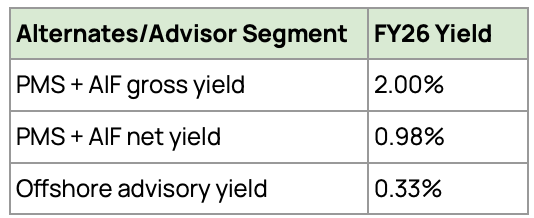

The alternates business further improves the company’s profitability. PMS and AIFs generated a strong 2.0% gross yield in FY26. Even after paying distributor commissions from the AMC’s own pocket, the company retained a healthy 0.98% net yield.

Offshore advisory is also attractive because it earns around 0.33% yield in a capital-light manner.

This shows that ICICI Prudential AMC is more inclined towards building a higher-margin platform, especially through PMS, AIFs and offshore advisory, than chasing AUM growth.

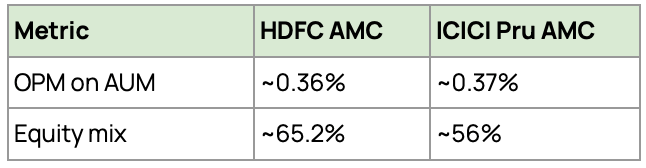

Despite having a slightly lower share of equity assets than HDFC AMC, ICICI Prudential AMC earns a slightly better operating profit margin.

A key reason appears to be the scheme-level mix.

As per ICICI AMC’s IPO document, HDFC’s equity AUM is more concentrated in a few large flagship schemes. Its top 5 equity schemes account for around 64% of equity AUM, compared with around 53% for ICICI.

Under SEBI’s telescopic TER structure, larger schemes move into lower expense-ratio slabs as AUM increases.

Asset management is a scale business, where the cost of managing additional AUM is low once the fund team, distribution network, compliance and technology platform are already in place. Large flagship schemes also have stronger investor recall and distributor familiarity, making them easier to sell and scale through. So even though bigger schemes may earn slightly lower TER under SEBI’s telescopic structure, HDFC benefits from lower product complexity, better operating leverage and a more predictable flow engine.

The real strength of a strong hybrid portfolio is visible during market corrections.

Between December 2025 and March 2026, when the Nifty 50 corrected 14.5%, and industry equity AUM declined 0.4% QoQ, ICICI Prudential AMC’s equity AUM still grew 2.0%, while its equity-oriented hybrid AUM grew 4.5%.

For the AMC, this is a clear business advantage. Sticky assets mean more predictable management fees, better revenue visibility and stronger resilience during downturns. So, apart from being a product strategy,

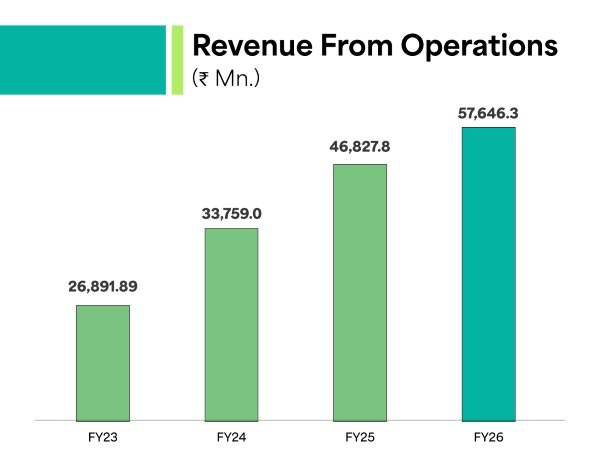

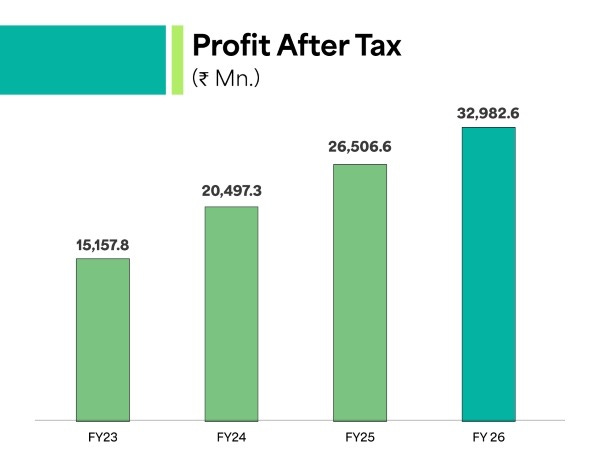

Coming to how ICICI Prudential AMC converts scale into cash…

Between FY23 and FY26, operating revenue increased from ₹2,689 crore to ₹5,764 crore, a CAGR of around 28.9%.

During the same period, PAT grew from ₹1,515 crore to ₹3,298 crore, a CAGR of around 29.6%.

The unit economics are also strong.

In FY26, the company earned a gross operating revenue yield of 0.52% on its annual average AUM. After deducting 0.038% of fees and commissions linked to the alternates business, the net operating revenue yield stood at 0.48%.

Also, operating expenses have steadily declined from 0.14% in FY24 to 0.12% in FY25 and further to 0.11% in FY26. As a result, the operating margin improved from 0.35% in FY24 to 0.37% in FY26.

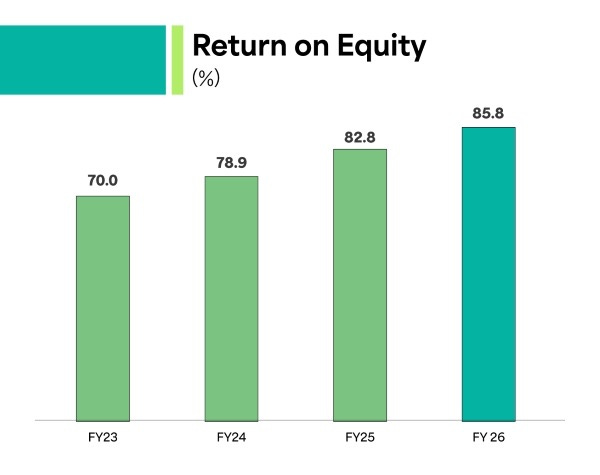

The AMC is debt-free. Since the business needs very little capital to grow, return ratios are exceptional, with ROE improving from 70.0% in FY23 to 85.8% in FY26.

Cash generation is visible in dividends as well. The business paid out most of its profits, with dividend payout remaining around 76-84% between FY23 and FY26. In FY26, it declared a dividend of ₹54 per share, with a payout ratio of 81.0%.

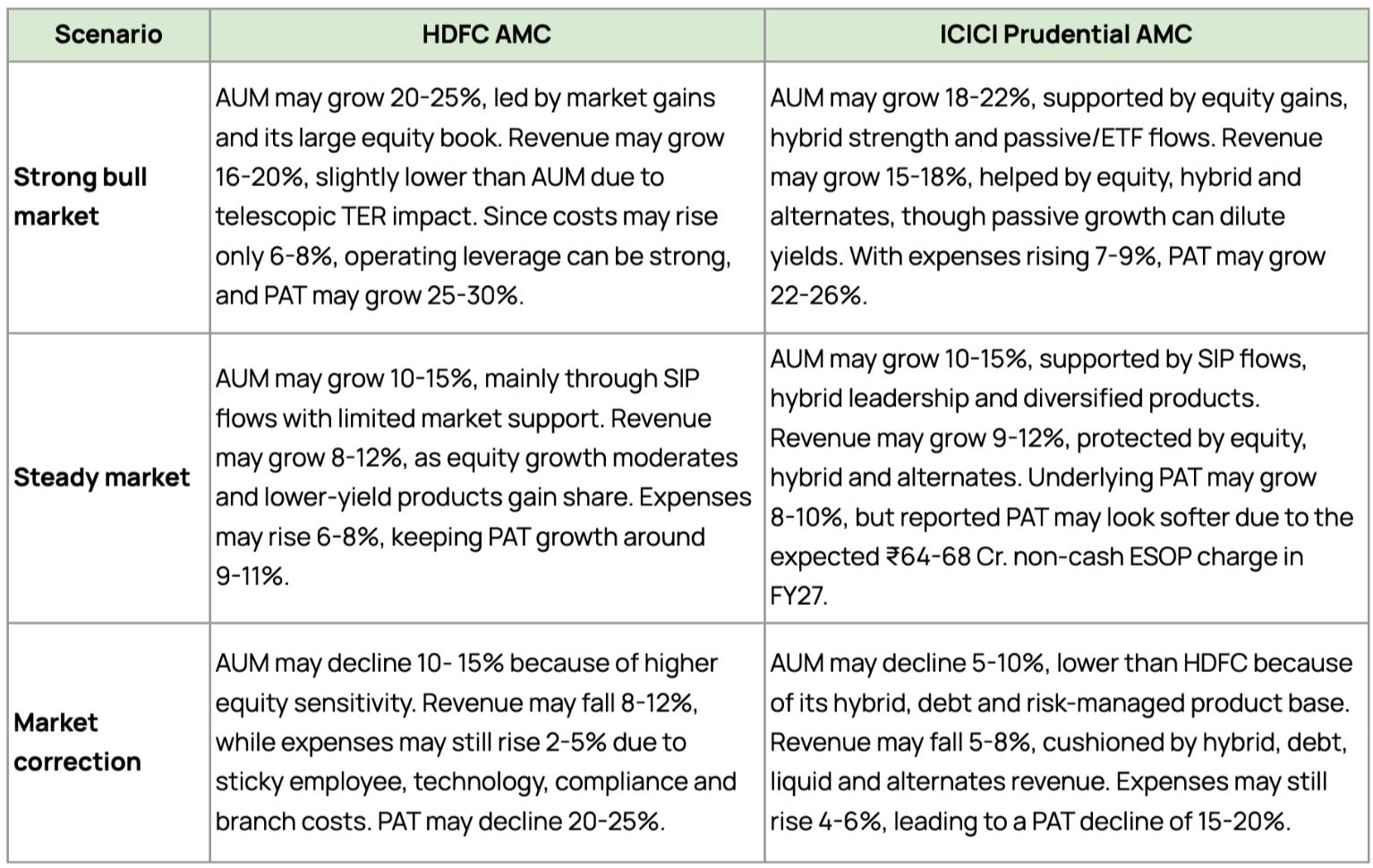

Rather than assume today’s conditions continue, let’s imagine three very different futures and see how the business responds to each.

HDFC AMC is more sensitive to equity markets because a large part of its AUM comes from equity-oriented funds. This helps the company in a bull market, as rising markets increase AUM and most of the extra revenue flows to profit because costs do not rise much. But in a weak market, the same equity exposure can hurt faster because AUM falls while employee, technology and compliance costs remain fixed in the short term.

ICICI Prudential AMC looks more balanced because its business is spread across equity, hybrid, passive and alternates. Its strong hybrid franchise can reduce downside during volatile markets, while the alternates business supports better yields.

However, rapid growth in low-yield passive funds can dilute margins, and the FY27 ESOP charge may put pressure on reported profit growth.

Overall, HDFC AMC offers stronger upside when equity markets are doing well, while ICICI Prudential AMC offers a more diversified and relatively stable model. For both companies, the key things to watch are fund performance, revenue growth versus AUM growth, TER pressure, passive mix and cost control.

Up to this point, we’ve looked almost entirely at why ICICI Prudential AMC has built such a strong franchise.

If this were all that mattered, investing would be easy.

The harder, and usually the more important part, is understanding what can break the thesis. Every company we study for Finology 30’s stock recommendations goes through the same exercise before we even think about valuation.

So, let’s look at the factors that could derail ICICI AMC’s growth:

Rise of DIY investing:

A structural risk for AMCs is the rapid rise of discount broker-led investing platforms. Platforms like Groww and Zerodha now have large active client bases, with Groww’s NSE active clients rising from around 56.5 lakh in June 2023 to 1.26 crore in June 2025. By May 2026, Groww had around 1.31 crore active clients, and Zerodha had around 68.5 lakh active clients. This shows that a large and growing pool of retail investors is becoming comfortable buying stocks, ETFs, IPOs and other market-linked products directly through broker apps.

Also, there is the rise of model portfolios and semi-DIY products like Smallcase. These platforms allow investors to buy curated baskets of stocks or ETFs based on themes and different strategies. This directly overlaps with categories like thematic, sectoral and active equity funds, where investors may feel they can create similar exposure with more transparency, direct ownership and greater control over the portfolio.

Faster growth of low-yield passive products:

In FY26, the AMC earned around 0.67% yield on equity funds, compared with only 0.10% on passive funds such as index funds and ETFs. This means passive AUM earns almost one-seventh of active equity AUM.

While equity schemes’ AUM grew 27.2% YoY, passive AUM grew 48.3% YoY to ₹1.84 lakh crore. If more investors shift from active funds to passive products, the company’s blended yield can come under pressure.

Regulatory fee compression:

Regulatory fee compression remains a structural risk for AMCs. From April 1, 2026, SEBI’s new expense framework has already led to around 3-4 bps gross yield compression for large AMCs on the existing book.

The actual P&L impact may be lower because large AMCs can partly offset this through distributor commission optimisation and cost control. However, the direction is clear: as SEBI pushes for lower investor costs, more transparency and tighter expense rules, blended yields can remain under pressure. Also, as schemes become larger, SEBI’s telescopic fee structure automatically lowers the expense ratio that AMCs can charge.

Fund-manager dependence:

ICICI Prudential AMC’s investment identity is closely linked with S. Naren, its Executive Director and CIO, who plays a central role in the fund house’s asset allocation and risk-managed investment philosophy.

Recent public data suggests that schemes associated with him account for over ₹3 lakh crore of AUM, spread across around 10 schemes.

Any eventual transition in his role, or weak performance in strategies closely linked to his investment style, can affect investor confidence, distributor conviction and flows into key active and hybrid products.

ICICI Prudential AMC operates in a highly competitive market, competing not only with large AMCs but also with new fund houses, fintech platforms, robo-advisory models, insurance products, and alternative investment products. As investor choices increase, sustaining flows will depend on fund performance, distribution strength, product innovation and trust.

The obvious next question is valuation.

A business can check every box and still be a poor investment if bought at the wrong price.

For an AMC, the P/E multiple approach is the most practical way to value the business. Unlike manufacturing companies, an AMC does not need heavy capital to grow. Once the fund management team, distribution network, compliance system and technology platform are in place, additional AUM can grow profits at a faster pace.

ICICI Prudential AMC is currently trading at around 50x trailing earnings, compared with the listed AMC peer average of around 40x. Since the stock is recently listed, we do not have a long valuation history to compare its current multiple.

On that basis, the stock is not cheap on headline valuation.

The market is already valuing ICICIAMC as a premium AMC franchise. This premium comes from its large scale, strong position in active equity funds, leadership in equity-oriented hybrid products, high return ratios and healthy dividend payout.

The market also seems comfortable valuing the company at around 40-45x forward earnings. This means investors are willing to pay a premium for ICICIAMC’s quality over debt or passive-heavy AMCs, and the long-term opportunity from the financialisation of Indian savings.

Putting all of this together…

HDFC AMC remains the cleaner equity-led franchise, with strong fund performance, low costs and a simple business model. But ICICI Prudential AMC seems to be the broader platform with much larger PMS, AIF and offshore advisory business. Its edge lies in hybrid and asset-allocation products, where it has built strong leadership and investor trust over many cycles.

Remember, though, while most businesses deserve analysis, very few deserve allocation.

Finology’s Exclusive Updates

From Ticker: The Aircraft Maintenance (MRO) Boom

While investors focus on airline stocks, India’s Aircraft Maintenance, Repair & Overhaul (MRO) industry is entering a multi-year growth phase. With GST cut to 5% and thousands of new aircraft on order, specialised engineering companies stand to benefit.

How to Spot MRO Winners on Ticker

Inventory Turnover Days: Falling inventory days signal faster parts movement and better cash flow.

CWIP Check: Rising Capital Work in Progress (CWIP) can indicate expansion of MRO infrastructure.

DuPont Analysis: Prefer companies with ROE driven by margins and asset efficiency, not debt.

Pro Tip: Airlines may battle on ticket prices, but every aircraft needs mandatory servicing. Use Ticker to find the engineering businesses enabling this structural growth.

That’s a Wrap for Today!

We’re always looking for interesting businesses and industries to explore.

If you enjoyed this DeepScan, we’d love to hear from you. And if there’s a company, industry, or business model you’d like us to break down next, simply reply to this email or drop a comment.

See you in the next edition!

Pranjal Kamra

Research: Jayesh Mohta

Editorial: Mehvish Qureshi

Disclaimer

The information and analysis provided herein are for educational and informational purposes only and do not constitute investment advice, a research recommendation, or an offer, solicitation, or recommendation to buy, sell, or hold any security. Investors should exercise their own judgment, conduct independent due diligence, and consult professional advisers before making investment decisions. Finology Ventures Private Limited, its affiliates, directors, employees, and research analysts shall not be liable for any loss or damage arising from the use of or reliance on this information.

SEBI Registered Research Analyst Details:

Registered Name : Finology Ventures Private Limited (RA Division)

Registration No : INH000024277

BSE Enlistment No. : 6877

Validity : Dec 16, 2025 - Dec 15, 2030