DeepScan #4: Prudent Corporate Advisory Ltd.

What makes it one of the biggest beneficiaries of India's mutual fund boom?

Hello!

Thank you for all the love you’ve shown the DeepScan series.

I wasn’t sure how many people would enjoy reading long breakdowns of businesses, so the response has been both gratifying and reassuring.

That tells there’s a genuine appetite for first-principles research. It’s the same process that eventually narrows thousands of listed stocks down to the 30 that we share through Finology 30 for long-term investors.

I’d love to hear what you think about it.

Onto today’s DeepScan…

If you’ve read our last 3 pieces on HDFC AMC, ICICI Prudential AMC and Nippon India AMC, today’s company is a natural next step. And if this is your first DeepScan, don’t worry, we’ll connect the dots as we go.

One thing I enjoy about studying businesses this way is that every company answers one question while raising another. After understanding how asset managers create investment products, the obvious next question becomes: who helps those products reach millions of investors?

Because India’s financialisation story doesn’t belong to asset managers alone.

Which brings us to Prudent Corporate Advisory Services.

As Indian households slowly shift their savings from physical assets, fixed deposits, and traditional savings products to formal financial products, many other businesses also benefit from the shift.

Mutual funds are only one part of a much larger ecosystem that makes investing possible, convenient and scalable for millions of people.

Asset management companies create the products.

Stockbrokers help investors participate in the market.

Stock exchanges and depositories provide the core infrastructure.

Registrar and transfer agents such as Computer Age Management Services and KFin Technologies manage investor records, transactions and servicing.

Wealth managers and distribution platforms take these products to the final customer.

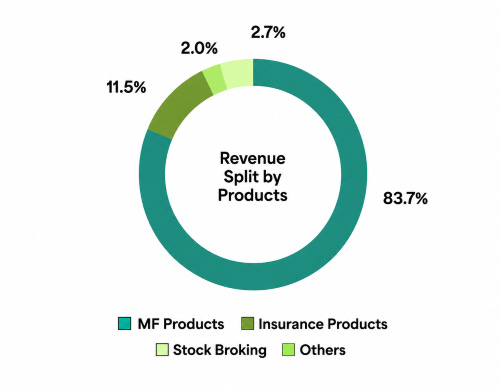

Prudent connects these financial products with investors.

It is a financial products distribution platform built largely around mutual funds. This is clearly visible in its revenue mix.

Before going deeper into Prudent, the most important question is:

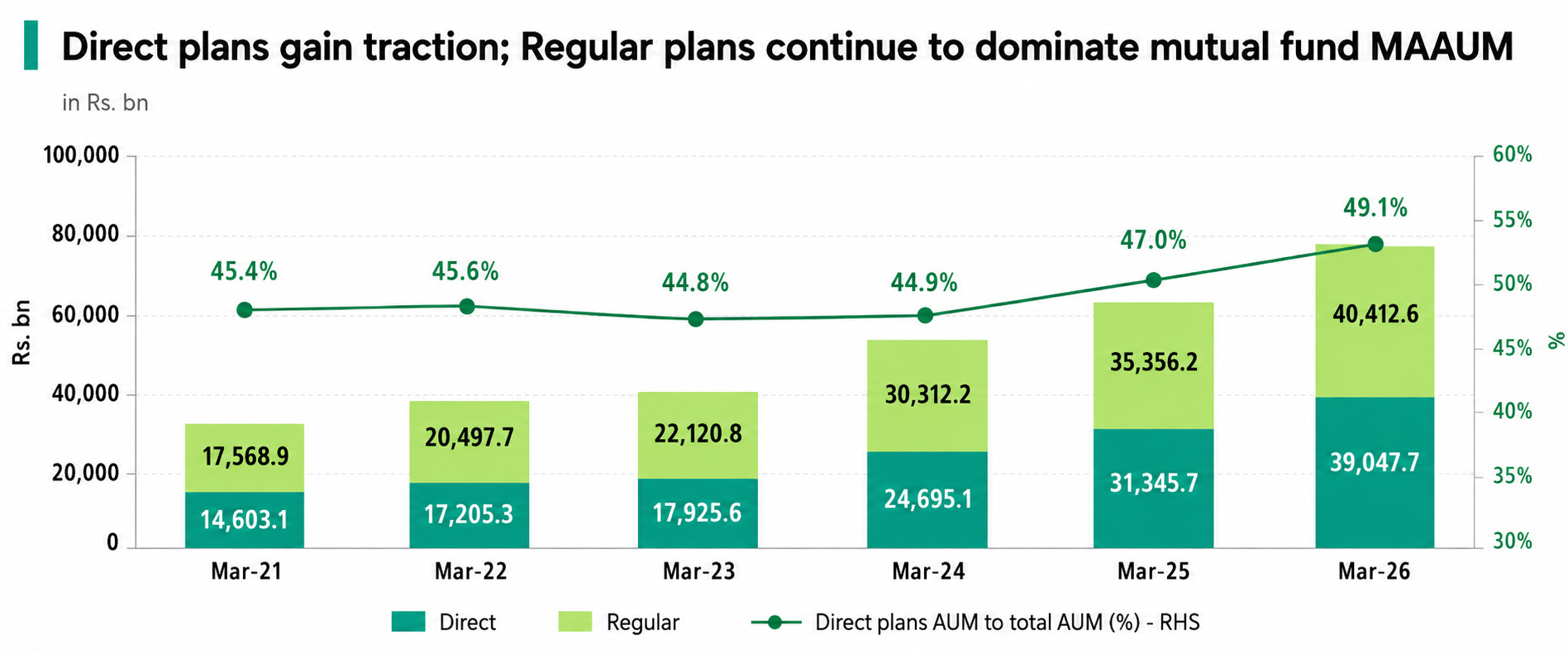

Are mutual fund distributors still relevant despite the rise of direct investing?

It is true that direct investing platforms are growing rapidly. Direct plans currently account for roughly 35% of the total monthly SIP inflows in the industry. This growth is largely driven by tech-savvy, do-it-yourself investors using fintech apps.

But this does not mean the distributor-led channel is becoming irrelevant. In fact, it remains one of the most important pillars of India’s mutual fund industry. Despite the rise of direct plans and digital investing platforms, around 71% of equity-oriented mutual fund assets still sit in regular plans. This means a large part of the industry still depends on distributors for investor acquisition, guidance and servicing.

Even a platform like Groww, which originally positioned itself around do-it-yourself direct mutual fund investing, has now entered the regular-plan/MFD model through Groww Prime.

The reason is simple.

Direct mutual funds help acquire users, but they do not create any income. Regular plans allow the platform to earn recurring commissions as the investor’s AUM grows through SIPs and market appreciation.

This shows why the MFD model remains economically attractive and why advice-led distribution still has value even for digital-first platforms.

Also, the real test of an investor comes during market volatility. During sharp market corrections, such as the one seen in March 2026, mutual fund distributors played an important role in hand-holding clients, preventing panic redemptions, and encouraging investors to continue their SIPs through rupee cost averaging.

This behavioural support makes a big difference. Investors in regular plans tend to stay invested for longer periods.

As of March 2026, about 35% of regular plan SIP assets had stayed invested for more than five years, compared with only about 20% for direct plans. In simple terms, distributor-led investors appear to exhibit greater persistence, while direct do-it-yourself investors are more likely to have shorter holding periods.

Another important opportunity lies in B-30 cities. While top-tier cities have seen faster digital adoption, investors in Beyond-30 cities still rely heavily on physical trust, local relationships and face-to-face guidance. These smaller, underpenetrated markets account for about 18.8% of industry AUM and remain a significant growth opportunity for the industry.

For these investors, the local mutual fund distributor is often the first point of trust. This makes the distributor-led model highly relevant outside large metro cities.

However, the MFD industry is highly fragmented.

India has roughly 1.98 lakh individual and corporate ARN holders. But the wealth is concentrated in the hands of a small set of large distributors. Only about 3,158 MFDs qualify as top distributors. This includes distributors with a presence in at least 20 locations, AUM of ₹100 crore or more, annual gross commission of at least ₹1 crore, or commission of ₹50 lakh or more from a single AMC. This is barely 2% of the total ARN base, and even within this group, the top 100 distributors control around 49% of regular-plan assets, showing how strongly the industry is concentrated at the top.

This creates a natural consolidation opportunity.

Running an independent MFD practice is becoming more difficult.

Challenge 1: Doing it all alone is getting expensive.

Smaller distributors now need to invest in technology, research, compliance, reporting systems and client servicing.

For many small MFDs, building all this independently is not easy. As a result, they are increasingly joining larger B2B2C platforms such as Prudent, which provide them with technology, product access, operational support and scale.

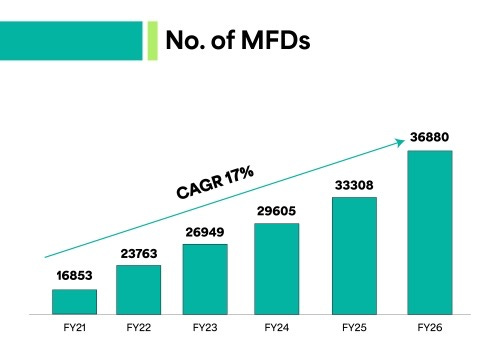

The numbers also show that Prudent added 3,572 net new mutual fund distributors (MFDs) in FY26, taking its partner base from 33,308 in March 2025 to 36,880 by March 2026.

Interestingly, the management also spoke about adding 5,100 new partners during the year. (The difference is because some partners also dropped off during the period, leaving the net addition at 3,572.)

What’s even more impressive? Prudent’s distributor network has grown at a 17% CAGR over the last five years. Today, nearly one in every five mutual fund distributors in India is empanelled with the company.

Challenge 2: Regulations have become tougher.

Earlier, mutual fund commissions from AMCs were paid inclusive of GST. This worked in favour of smaller distributors who weren’t GST-registered. They could simply keep the entire commission, while GST-registered distributors had to deposit the tax.

That changed in April 2026. Commissions are now paid exclusive of GST, meaning non-GST distributors no longer get that extra benefit. Their effective earnings could decline by 15-20%, making larger platforms like Prudent more appealing for their compliance and operational support.

Challenge 3: Commission pools are shrinking.

Along with GST changes, another pressure point is the removal of the old 0.05% exit-load-linked TER benefit.

In simple terms, the overall fee pool within mutual fund schemes has become slightly smaller. If AMCs pass on this reduction, distributors could see their trail commissions dip by a few basis points. Prudent estimates the impact on its existing book at around 0.02-0.03%, which it may partly absorb by sharing it with its distributor partners.

For small independent MFDs, this makes the economics slightly tougher because even small cuts directly reduce their recurring trail income.

This pressure is pushing smaller MFDs towards larger aggregator platforms, where they can reduce their operational burden and focus more on client relationships.

Challenge 4: Who takes over the business?

A large number of MFDs who started their practices decades ago are now in their late fifties or sixties. Many of them do not have a clear succession plan, as the next generation often chooses different careers.

These traditional MFD businesses were also not always built on scalable digital processes.

As a result, many retiring MFDs are increasingly open to selling their businesses or partnering with larger organised platforms. This helps them protect client continuity while also monetising the practice they have built over decades.

The role of MFDs is also expanding beyond reach for some.

Earlier, many distributors were mainly mutual fund sellers. Today, clients expect much more. They want broader financial planning, asset allocation, insurance advice, tax-efficient products and access to multiple investment options.

This is forcing MFDs to upgrade from being simple mutual fund distributors to becoming full-fledged wealth managers. Their product basket now needs to include life insurance, health insurance, PMS, AIFs, fixed deposits and other financial products.

This again favours large multi-product platforms such as Prudent.

A small independent MFD may find it difficult to offer such a wide product suite, technology support and servicing capability on its own. But by joining a larger platform, the distributor can offer more products, improve client servicing and remain relevant in a changing market.

TLDR: Direct platforms will continue to grow among younger, digitally comfortable investors. But for a large part of India, especially in smaller cities and among investors who need guidance, trust and behavioural support, the distributor-led model remains important.

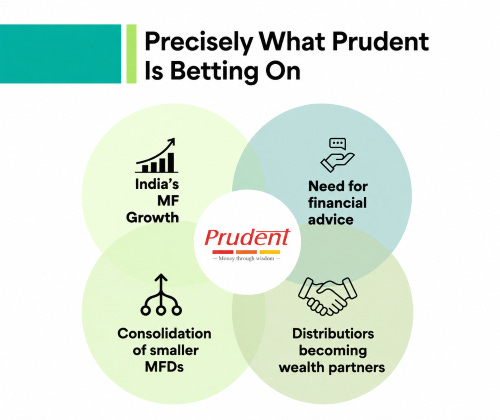

Think of Prudent as a business benefiting from four powerful trends shaping India’s financial services industry.

Now take a look at these images:

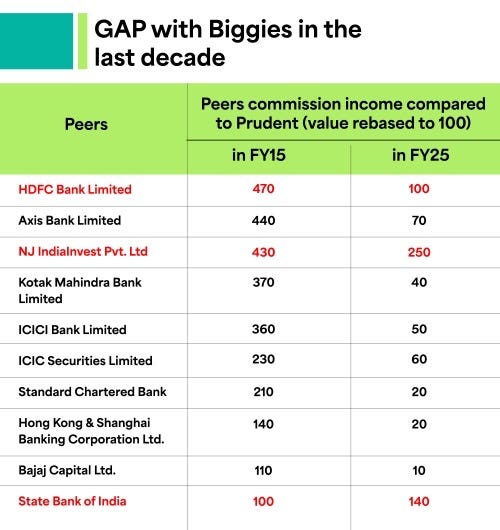

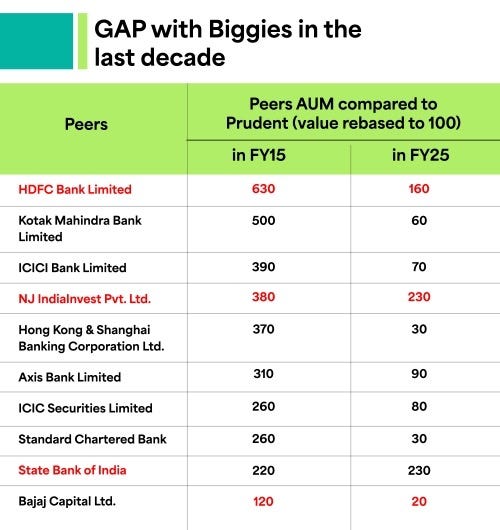

As of 2026, Prudent is the second-largest non-bank mutual fund distributor in India, behind NJ IndiaInvest. If large banks are also included, Prudent ranks fourth overall in terms of commission earned.

However, what makes Prudent interesting is not just its current position, but the speed at which it has grown.

In FY15, for every ₹100 of commission income earned by Prudent, NJ earned ₹430. This means NJ was around 4.3 times larger than Prudent. By FY25, this gap had reduced sharply. For every ₹100 in commission earned by Prudent, NJ earned ₹250, reducing the gap from 4.3 times to 2.5 times.

The same trend is visible in AUM as well.

In FY15, for every ₹100 of AUM on Prudent’s platform, NJ had ₹380, meaning the AUM gap was 3.8 times. By FY25, NJ’s AUM stood at ₹230 for every ₹100 of Prudent’s AUM, reducing the gap to 2.3 times.

Prudent has also gained a relative share versus most bank-led distributors over the last decade. In FY15, large banks such as HDFC Bank, Axis Bank, Kotak Mahindra Bank and ICICI Bank were 3.6 to 4.7 times Prudent’s commission income.

By FY25, most of them were either at par with Prudent or meaningfully below it. The same trend is visible in AUM, where the gap with most private and foreign banks has compressed sharply.

This means…

Prudent has grown faster and steadily gained ground against the larger player. Below are the key reasons:

Prudent built its technology around the needs of independent mutual fund distributors. FundzBazar helped MFDs onboard clients, start SIPs, process transactions, generate reports and service investors more efficiently. This is why Prudent’s top distributors grew AUM at around 36% CAGR over the past decade, compared with roughly 17% CAGR for the broader industry’s top 1,000 distributors.

In comparison, NJ’s top 1,000 partners also grew strongly, with AUM compounding at 26.62% over FY15 to FY25.

It also combined its digital tools with a physical branch network of around 144 locations, giving it a strong “phygital” presence. This helped the company build trust and capture assets from smaller towns (B30 locations), which now contribute around 22% of its total assets. In a business where relationships still matter, this mix of technology plus ground presence became a key growth driver.

Prudent also used acquisitions to add scale quickly. It acquired distribution books such as iFast with ₹517 crore of assets and Indus Capital with ₹2,104 crore of assets.

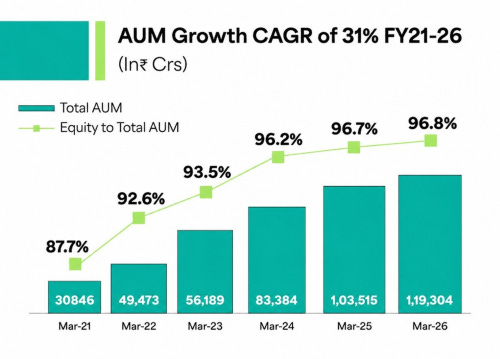

This technology-led growth is visible in Prudent’s own numbers as well.

Between FY21 and FY26, Prudent’s mutual fund assets increased from ₹30,846 crore to ₹1,19,304 crore, implying a CAGR of around 31%. Its equity AUM ex-ETF market share also improved to 2.61% in March 2026, compared with 2.52% in March 2025.

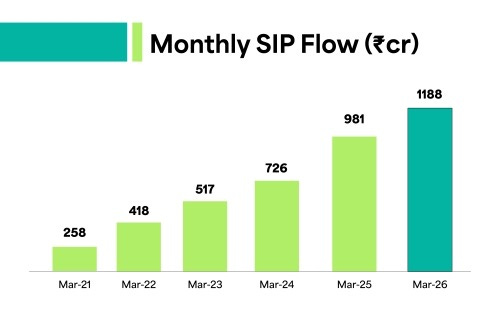

Over the same period, its monthly SIP flow increased from ₹258 crore to ₹1,188 crore, implying a CAGR of around 36%. This shows that growth is not only coming from market movement.

The platform is also adding regular monthly flows through SIPs. More importantly, its SIP market share has remained strong, rising from around 3.6% in March 2025 to 3.65% in March 2026.

So, the SIP book matters a lot in this business.

For an asset management company, SIPs are a source of sticky AUM. For a distributor like Prudent, SIPs are even more important because they keep the distributor connected with the investor every month.

A lump-sum investor may come once and disappear. A SIP investor stays in the system, receives reviews, needs servicing, and can be cross-sold other financial products over time.

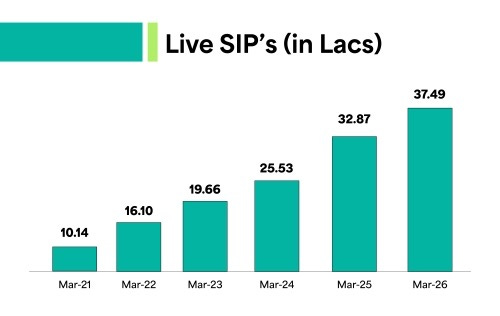

This is why the growth in live SIPs is important. Prudent had 37.49 lakh live SIPs by March 2026, compared with 10.14 lakh in March 2021. That implies a CAGR of around 30% in live SIPs over FY21 to FY26.

Prudent’s model benefits from two types of growth.

The first is AUM growth from existing distributors. As their clients invest more, Prudent’s assets and trailing income grow.

The second is distributor addition. As more independent distributors join Prudent’s platform, the company gets access to new clients, new flows and new geographies without directly hiring every relationship manager itself.

This brings us to the next layer of Prudent’s model: Cross-Selling.

Insurance is already Prudent’s second-largest vertical, but it is still built on top of the mutual fund distribution engine.

In FY26, insurance revenue stood at ₹152 crore, compared with ₹36.1 crore in FY22. That is more than 4 times the growth in four years, implying a CAGR of around 43%. Insurance now contributes around 11.5% of Prudent’s FY26 revenue, compared with 7.2% in FY20.

The growth has mainly come from using the existing mutual fund distributor network better. Out of Prudent’s 36,880 mutual fund distribution partners, 13,386 are also empanelled as Point-of-Sale Persons for insurance.

This is important because Prudent is not trying to build a completely separate insurance distribution network but rather to cross-sell insurance through the same trusted distributor base that already serves mutual fund investors.

Other products are still small but optional.

Prudent’s non-mutual-fund, non-insurance businesses include stock broking and other financial products such as portfolio management services, alternative investment funds, bonds, fixed deposits, Smallcase portfolios, the National Pension System, unlisted securities and loans against securities.

Together, these products give Prudent a wider wallet-share opportunity from the same customer and distributor base.

Stock broking has not really scaled meaningfully. Revenue from stock broking and allied services was ₹23.5 crore in FY22 and ₹27 crore in FY26.

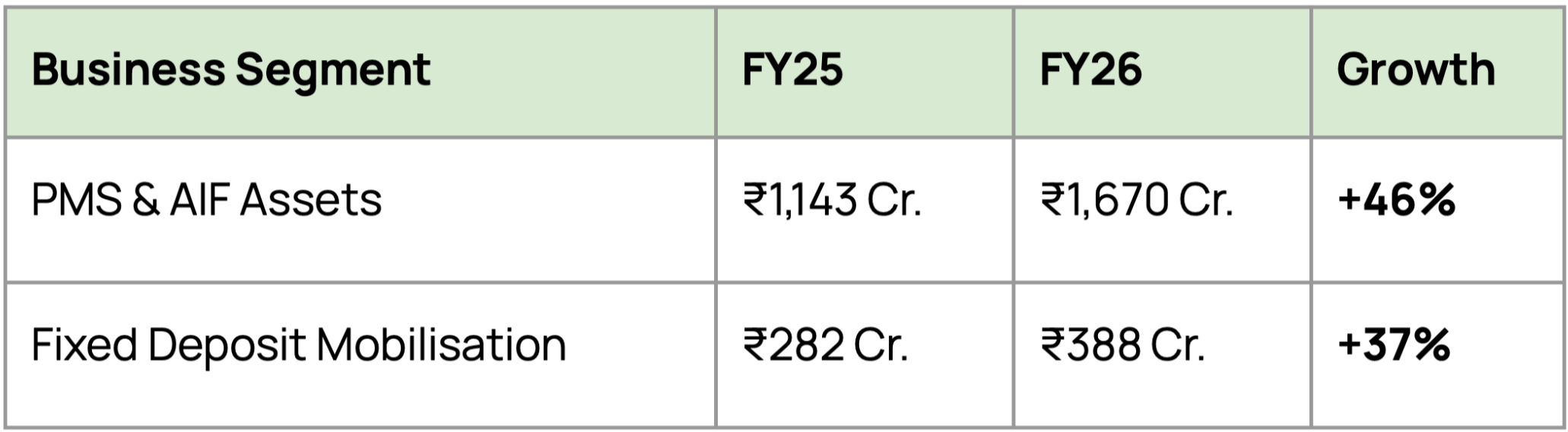

The more interesting optionality is in other financial products. Revenue from this bucket increased from ₹7 crore in FY22 to ₹33.4 crore in FY26, implying around 48% CAGR. This segment includes portfolio management services, alternative investment funds, fixed deposits, bonds, Smallcase portfolios and loans against securities.

Within this, portfolio management services and alternative investment fund mobilisation contributed around 66% of segment revenue, fixed deposits contributed around 18%, and the rest came from other products.

The company’s other financial products are growing as well.

Key mental model to remember?

The mutual fund business brings distributor relationships, investor trust, and recurring trail income. Insurance, PMS, AIFs, fixed deposits and other financial products can then be layered on top of the same network.

This makes Prudent more than just a mutual fund distributor. It is becoming a platform for smaller distributors who want technology, products, research, compliance support and scale, without losing their client relationships.

Coming to how Prudent converts scale into profits….

This is usually the point where most businesses get filtered out during our research for Finology 30’s stock recommendations. A great industry and a growing business aren’t enough. We also want to know how that growth eventually translates to revenues, profits and cash flows.

Prudent’s mutual fund commission yield (net of GST) is around 0.91% on AUM, which means it earns roughly ₹0.91 per year for every ₹100 of average mutual fund assets distributed through its platform.

In FY25 AMFI gross commission data, Prudent’s yield was around 1.06% including GST, broadly comparable to NJ IndiaInvest’s 1.15% and much higher than large bank distributors such as SBI at 0.66% and HDFC Bank at 0.70%.

This higher yield is mainly because Prudent’s book is heavily equity-oriented, with 96.8% of AUM in equity-oriented schemes, where trail commissions are structurally higher than debt, liquid or passive products.

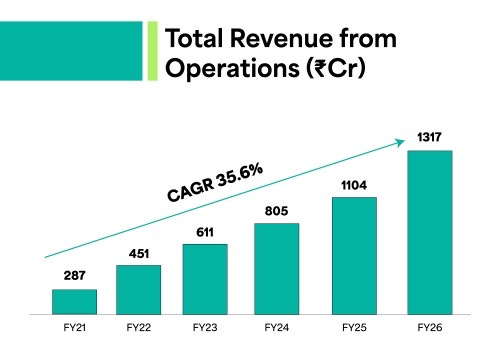

Between FY21 and FY26, Prudent’s revenue from operations increased from ₹287 crore to ₹1,317 crore, implying a CAGR of around 35.6%.

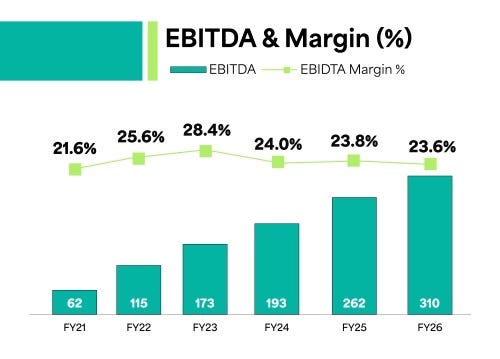

Over the same period, EBITDA increased from ₹62 crore to ₹310 crore, a CAGR of around 38%.

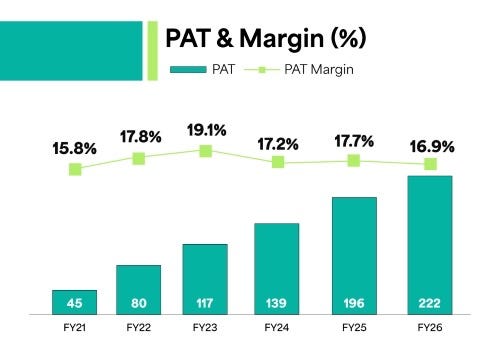

While profit after tax increased from ₹45 crore to ₹222 crore, a CAGR of around 38%.

So, unlike an AMC, Prudent does not show sharp margin expansion as it scales. Its operating profit margin was 25.6% in FY22 and 23.6% in FY26. This is because Prudent receives commissions from AMCs and then shares a large portion of those commissions with its MFD partners.

In FY26, revenue from operations grew 19.4%, while commission and fee expenses grew almost in line at 19.8%. In simple words, Prudent has operating leverage in technology, servicing and corporate costs, but not the same level of margin leverage as an AMC, because distributor payouts remain a high variable cost.

However, the business is still highly profitable and capital-light. Return on equity remained strong at 28.7% in FY26, and the company has averaged around 35% ROE in the last 5 years.

Has management walked the talk?

Prudent also did a good job of delivering on what it had promised at the start of the year.

Management had guided for mutual fund distribution yields to stay around 90 bps, despite the impact of back-book repricing. It ended FY26 at 91 bps, marking the third straight year with broadly stable yields.

It also came remarkably close to its ₹1,200 crore monthly SIP target for March 2026, finishing at ₹1,188 crore, missing the target by just ₹12 crore, or 1%. Even so, the SIP book expanded by ₹209 crore during the year, taking its SIP market share to 3.65%.

Just as importantly, the company kept distributor payouts under control. Commission and fee expenses grew 19.8% in FY26, almost in line with the 19.4% growth in revenue from operations, suggesting that payout discipline remained intact.

The Indus Capital integration has also started well. Of the ₹2,104 crore AUM announced at acquisition, around ₹2,060 crore was transferred to Prudent, which grew to approximately ₹2,250 crore by May 2026. All relationship managers were retained.

That said, it’s still too early to call the ₹123.75 crore acquisition a success. The real test will be long-term client retention, net flows and returns on the capital invested.

Overall, management met most of the FY26 targets.

It maintained commission yields,

kept distributor payouts under control,

nearly achieved its SIP target, and

integrated Indus Capital well.

Would you say Prudent's biggest challenge is likely to come from inside the business or outside it?

The business is not without fault lines. The same model that gives Prudent scale also leaves it exposed to market cycles, fee regulation, distributor economics and the gradual shift toward direct investing.

The most persistent structural threat to Prudent…

It’s the continuous regulatory pressure on its commission yields. In the mutual fund industry, a distributor’s income is constantly fighting a downward pull known as “back-book repricing“. As a mutual fund scheme grows larger, the market regulator, SEBI, forces the asset management company (AMC) to lower the total expense ratio (TER) it charges investors. When the AMC collects less, it automatically cuts the trail commissions it pays to platforms like Prudent on those older, accumulated assets.

Furthermore, SEBI frequently introduces new rules that compress the overall fee pool. For example, recent regulatory proposals include the removal of a 0.05% exit load benefit and reductions in allowable brokerage costs. Combined, these changes are expected to reduce overall industry expense ratios by roughly 0.06%-0.07%. While AMCs, brokers, and platforms will share this burden, it will squeeze the gross yields Prudent can earn.

Another major structural headwind is the accelerating shift towards do-it-yourself (DIY) direct investing and the rise of passive investing, which we discussed in detail in Nippon Life’s DeepScan.

Now, because of this, the regular plan segment is structurally losing its overall market share within the broader industry.

While Prudent has successfully gained market share within the regular distribution space to offset this, the overarching reality remains that a growing segment of tech-savvy, cost-conscious investors is permanently bypassing distributors altogether.

Even within the regular distribution space, Prudent faces structural risks regarding its net profitability due to rising competitive intensity.

Prudent’s B2B2C model works by retaining a spread; it earns a gross commission from the AMC and passes a large portion down to its independent mutual fund distributors. Historically, Prudent has paid out roughly 64% of its gross revenue on a normalised basis, or roughly 67-68% within its indirect mutual fund channel.

However, several new private equity-backed B2B2C platforms have recently entered the market, aggressively trying to lure distributors away by offering significantly higher commission payouts, sometimes ranging from 85% to 90%.

If these well-funded competitors persist, Prudent may eventually be forced to increase its payout ratio to retain its top distributors, which would permanently compress its profit margins.

What about the valuations?

Well, at the current valuation, Prudent is pricing in a fairly strong growth outcome. The stock trades at around 55x earnings, compared with its historical median of roughly 45x. If the multiple normalises back to 45x over the next five years, and an investor still wants a 15% annual return, Prudent’s PAT will need to grow from ₹222 crore in FY26 to around ₹545–550 crore by FY31. That implies a required PAT CAGR of nearly 20%.

It does not look unrealistic if the broader mutual fund industry continues to grow well from low penetration levels.

Prudent is positioned in the right part of the value chain, where equity AUM, SIP flows and distributor-led assets can keep compounding over the long term. Its technology-led platform, wide MFD network, and strong distribution support also make it well-placed if smaller distributors continue to consolidate toward larger, organised platforms.

The other comfort is that Prudent is less exposed to the performance risk of any single AMC because its AUM is spread across multiple fund houses. It also has some ability to manage regulatory pressure, as past commission cuts were partly passed on to distributors, while newer flows can come at better yields. So, while the stock valuation already demands strong execution, a 20% PAT growth assumption looks achievable if industry growth remains healthy, Prudent keeps gaining share, and distribution economics do not deteriorate sharply.

In our view..

Prudent is the cleanest listed play on India’s mutual fund distribution theme. The core thesis is simple: if equity mutual fund penetration, SIP culture and MFD platformisation continue to grow, Prudent should remain one of the key beneficiaries.

Finology’s Exclusive Updates

From Ticker: Premium Spirits & The Single Malt Boom

While mass-market alcohol volumes are flattening, India’s premiumisation wave is creating a major value opportunity. As disposable incomes rise, consumers are upgrading to premium single malts and craft spirits, allowing specialised distilleries to earn far higher margins than legacy value brands.

How to spot the winners on Ticker:

P&A Shift: Check investor presentations for a rising Prestige & Above mix—a sign of pricing power.

OPM Expansion: Track Operating Profit Margin over the last 4 quarters to confirm premium-led margin growth.

DuPont Analysis: Verify that high ROE comes from stronger profit margins, not debt.

Mass volumes may be flat, but premium value is booming. Use Ticker to identify distilleries successfully shifting towards luxury portfolios before the market fully prices in the opportunity.

That’s a Wrap for Today!

We’re always looking for interesting businesses and industries to explore.

If you enjoyed this DeepScan, we’d love to hear from you. And if there’s a company, industry, or business model you’d like us to break down next, simply reply to this email or drop a comment.

See you in the next edition!

Pranjal Kamra

Research: Jayesh Mohta

Editorial: Mehvish Qureshi

Disclaimer

The information and analysis provided herein are for educational and informational purposes only and do not constitute investment advice, a research recommendation, or an offer, solicitation, or recommendation to buy, sell, or hold any security. Investors should exercise their own judgment, conduct independent due diligence, and consult professional advisers before making investment decisions. Finology Ventures Private Limited, its affiliates, directors, employees, and research analysts shall not be liable for any loss or damage arising from the use of or reliance on this information.

SEBI Registered Research Analyst Details:

Registered Name : Finology Ventures Private Limited (RA Division)

Registration No : INH000024277

BSE Enlistment No. : 6877

Validity : Dec 16, 2025 - Dec 15, 2030

Sir ye hindi me nhi h