ETFs Are Not as Cheap as You Think

It is not the expense ratio.

There is a number that almost every ETF advertisement leads with. The expense ratio. It is low, sometimes lower than the equivalent index fund, and it is presented as the primary reason to choose an ETF over any other investment vehicle.

That number is real but also incomplete. And the part it leaves out is costing retail investors significantly more than most of them realise.

What You Are Actually Paying

The expense ratio only captures what the fund house charges you to manage the money. It does not capture what it costs you to buy and sell the ETF itself. When you add both together, the Total Ownership Cost of an ETF is typically between 0.7% and 1% annually. That is often higher than the total cost of owning a comparable index fund.

To understand where that extra cost comes from, you need to understand how ETFs actually work.

How You Buy an ETF vs How You Buy an Index Fund

When you invest in an index fund, the transaction is direct. You send money to the fund house, they issue you units at that day’s NAV, and every rupee you invest goes to work immediately. The fund house guarantees your liquidity when you want to exit.

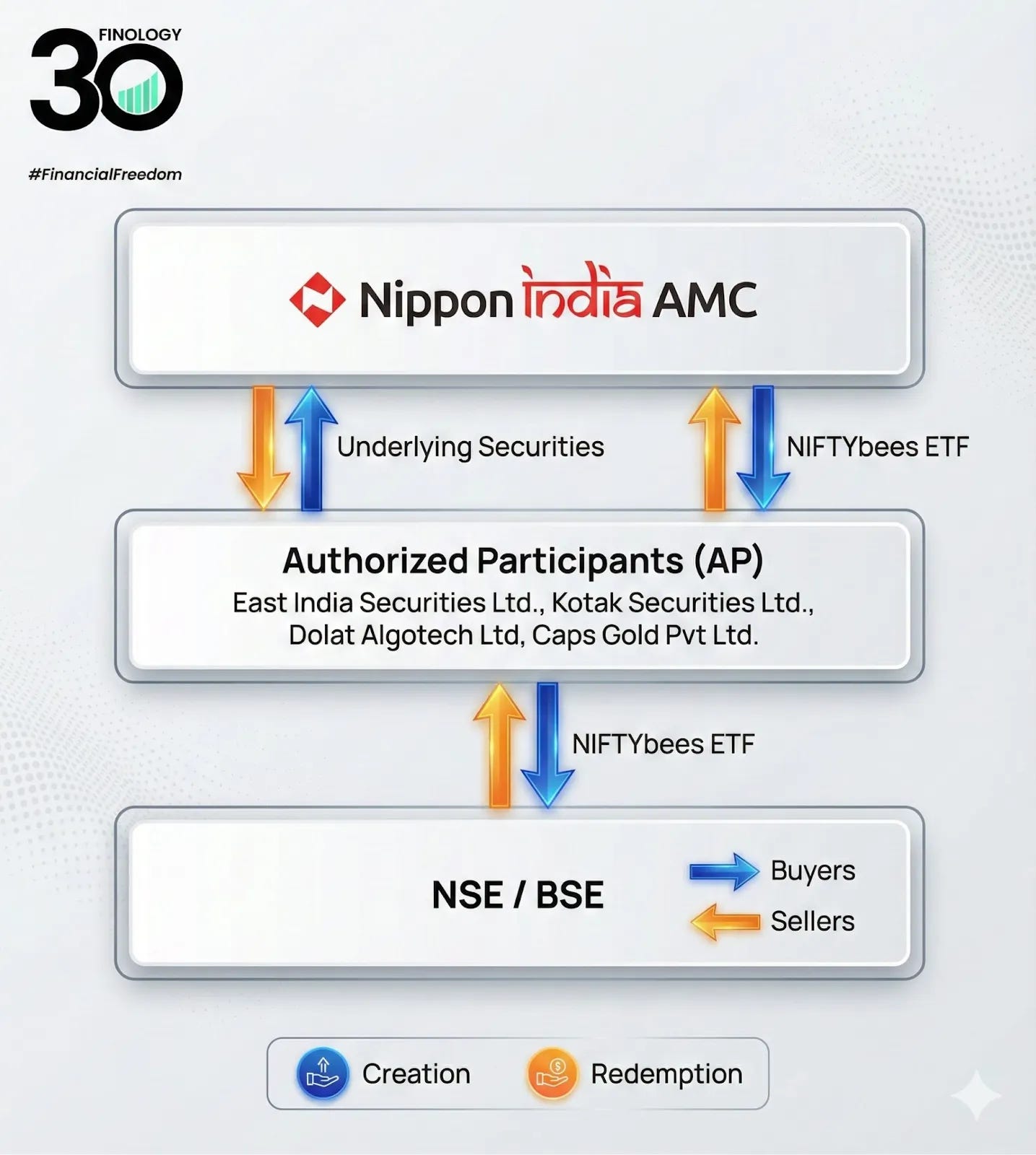

ETFs work differently. The fund house does not sell units directly to retail investors. Instead, they create large blocks of units and hand them to intermediaries called Authorised Participants (APs) typically large broker-dealers or market makers officially appointed by the AMC. These intermediaries then sell those units to you on the stock exchange.

Because the fund house steps back from the transaction entirely, the liquidity you need to buy and sell is provided not by the AMC but by these middlemen. And middlemen, naturally, charge for that service.

The Bid-Ask Spread: Your Hidden Cost

APs make their money through what is called the bid-ask spread. At any given moment, they are quoting two prices on the exchange: the price at which they will buy units from you, and the slightly higher price at which they will sell units to you. The gap between those two prices is what they pocket on every transaction.

Here is a concrete example. Say an ETF’s actual NAV is ₹100. The APs buys the underlying stocks for ₹100, converts them into ETF units, and lists them on the exchange at ₹105. You buy at ₹105. The AP pockets the ₹5 difference.

You just paid ₹105 for an asset worth ₹100. That five rupee gap is your hidden entry cost, and it happens in reverse when you sell. You sell at the bid price, which is lower than the NAV, and the AP pockets that difference too.

This happens on every single transaction. For an investor running an ETF SIP with a market order, which is how most retail investors do it, this cost compounds quietly and consistently over time.

Why ETFs Were Designed This Way

If mutual funds already exist and work cleanly, why create this more complicated structure at all?

The honest answer is that ETFs were designed to solve a problem that institutional investors and fund managers face, not one that retail investors face.

In a mutual fund, when a large investor redeems a significant amount, the fund manager has to sell stocks to generate that cash. Those transactions create costs and tax consequences inside the fund that every remaining investor absorbs. It is an invisible tax on the people who stayed.

ETFs solve this elegantly for the fund manager. When you sell your ETF units, you simply trade them with another buyer on the exchange. The fund manager does nothing. The underlying portfolio stays completely untouched. No transaction costs, no tax leakage, no disruption.

The fund manager’s problem is solved. Yours is not. The liquidity burden has simply been transferred from the AMC to you, and you bear it every time you buy or sell.

So When Do ETFs Make Sense?

ETFs are not universally bad. For large institutional investors who can transact in block sizes that minimise the spread, or for investors making very infrequent lump sum investments where the one-time spread cost is negligible, ETFs can be the right choice.

For a retail investor running a monthly SIP, paying the bid-ask spread on every single contribution, the cost arithmetic often favours a direct index fund instead. The expense ratio on the index fund might be marginally higher. The total ownership cost is frequently lower.

The ETF industry leads with the expense ratio because it is the number that looks best. The total ownership cost is the number that actually matters. Before your next investment decision, make sure you are looking at the right one.